Have you noticed FPO on a bank statement and wondered whether it is something you should be concerned about?

The FPO usually stands for Faster Payment Outward, which means money has been sent from your account to another account through the UK Faster Payments system. It is a standard banking reference used by UK financial institutions and, in most situations, simply reflects a transfer you authorised.

Understanding transaction codes helps you read your statement with greater confidence and quickly spot anything unusual.

Key points to know:

- FPO normally means money leaving your account

- It refers to a transfer processed through Faster Payments

- Payments are often completed within seconds or minutes

- Unknown FPO entries should always be reviewed promptly

Bank statements can look technical at first glance, but understanding terms like FPO makes managing your finances significantly easier.

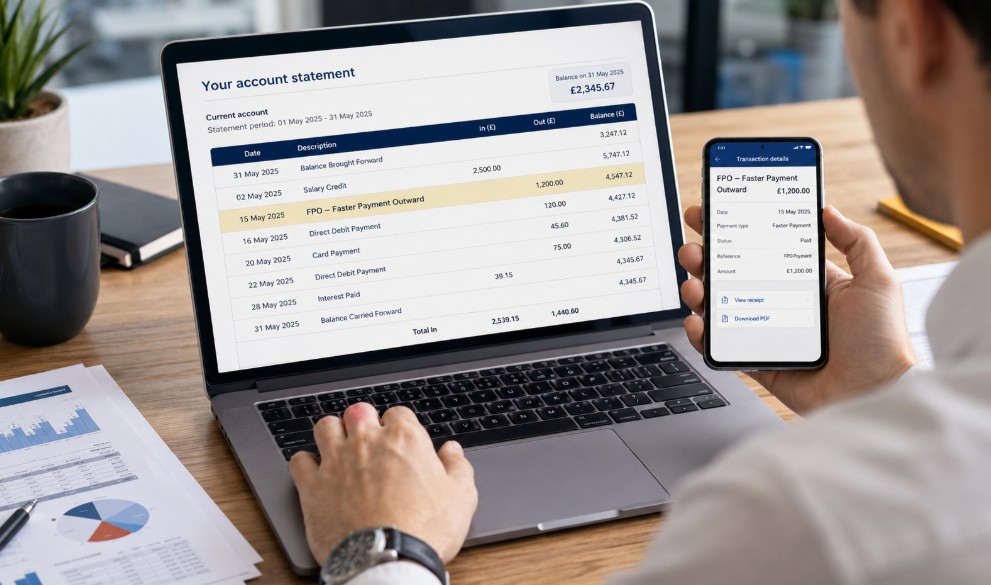

What Does FPO Mean on a Bank Statement?

When you see FPO on a bank statement, it generally means Faster Payment Outward (sometimes displayed as Faster Payments Outwards depending on the bank).

This indicates that money has been transferred electronically from your bank account to another account using the UK’s Faster Payments Service (FPS).

The Faster Payments network was introduced to make transfers quicker and more convenient compared with older payment methods. Today, it is one of the most commonly used payment systems across personal and business banking in the UK.

Unlike card transactions, Faster Payments move directly between bank accounts and often complete almost instantly.

Understanding Faster Payment Outward (FPO)

The term itself can be broken down simply:

- Faster Payment → Payment processed through the Faster Payments network

- Outward → Funds leaving your account

This means FPO is generally recorded as a debit transaction.

“Faster Payments transformed UK banking by enabling near real-time transfers while maintaining robust security controls.” — UK Payments Infrastructure Representative

How FPO Typically Appears on UK Bank Statements?

Banks may present FPO transactions differently depending on their statement format.

Transaction examples:

| Statement Entry | Meaning |

| FPO JOHN SMITH | Payment sent to named recipient |

| FPO INV-4021 | Payment linked to invoice reference |

| Faster Payment Out | Outgoing Faster Payment |

| FP Transfer | Bank transfer processed electronically |

You may also see additional references beside the transaction that help identify the recipient.

Although labels vary slightly, the underlying meaning remains broadly the same: the payment was sent from your account.

Why Is FPO Showing on Your Bank Statement?

If FPO appears on your statement, it usually means you recently completed a transfer through online banking, mobile banking, or another electronic payment channel.

Most people encounter FPO during normal financial activity and do not realise that bank statements shorten transaction descriptions.

Common situations that generate an FPO entry include sending rent, transferring money to family members, paying suppliers, settling invoices, or moving funds between accounts.

Examples of everyday FPO usage:

- Paying household bills manually

- Sending money to friends

- Paying credit card balances

- Moving savings between accounts

- Paying contractors or freelancers

- Completing one-off online transfers

Businesses also rely heavily on Faster Payments because of their speed and convenience.

If the timing and amount match your recent activity, the transaction is usually nothing to worry about. Understanding how these references appear makes reviewing statements easier over time.

Is FPO on a Bank Statement Money Going Out or Coming In?

In most cases, FPO on a bank statement means money is going out of your account. The abbreviation is commonly used by UK banks to indicate that funds have been transferred electronically through the Faster Payments Service (FPS) to another account.

Many customers become confused because bank statements often display multiple abbreviations that look similar at first glance. Understanding these transaction labels can make it easier to read your statement accurately and avoid unnecessary concern.

FPO vs FPI: Understanding the Difference

Although FPO and FPI are closely related, they indicate opposite directions of payment movement.

FPO vs FPI Comparison:

| Code | Full Meaning | Money Direction |

| FPO | Faster Payment Outward | Leaving your account |

| FPI | Faster Payment Inward | Entering your account |

If someone transfers money to you through the Faster Payments network, your statement may display FPI instead of FPO. This distinction helps identify whether funds were sent or received.

Understanding the difference becomes especially useful when reviewing recent transfers or checking whether expected payments have arrived.

Common Payment Directions Explained

Outgoing payments reduce your available balance, while incoming payments increase it. Recognising the direction of a transaction can help you understand account activity more quickly.

Examples include:

- Paying a landlord → FPO

- Receiving a salary reimbursement → FPI

- Sending money to a savings account → FPO

These examples show how the same payment system can support both incoming and outgoing transfers depending on the transaction.

Transaction Types You May See Alongside FPO

When reviewing your statement, you may notice several other abbreviations appearing alongside FPO transactions. These codes identify how a payment was processed.

Common UK Bank Statement Codes:

| Code | Meaning |

| DD | Direct Debit |

| SO | Standing Order |

| CHG | Bank Charge |

| ATM | Cash Withdrawal |

| POS | Card Purchase |

Learning these common references makes account monitoring easier and allows you to identify unusual activity more efficiently. Over time, becoming familiar with transaction codes can help you manage your finances with greater confidence.

What Transactions Usually Create an FPO Entry on a Bank Statement?

An FPO entry can appear on a bank statement after many everyday banking activities. It usually relates to a payment sent directly by the account holder through online banking or a mobile banking app.

One-off transfers are the most common reason because the money is actively sent rather than collected automatically.

Common transactions that may create an FPO entry include:

- Paying household bills manually

- Transferring money between your own accounts

- Sending money to friends or family

- Paying service providers or tradespeople

- Making deposits or account transfers

- Paying freelancers, suppliers, or business invoices

Because Faster Payments are processed quickly, the transaction may appear almost immediately on your statement.

This makes banking more convenient, but it also means you should check payment details carefully before confirming any transfer

How Is FPO Different from Direct Debit, Standing Order, BACS and CHAPS?

Although these payment methods all transfer money between accounts, they work in different ways and serve different purposes.

Understanding the differences helps you interpret FPO on bank statement entries more accurately and choose the right payment option when managing your finances.

An FPO (Faster Payment Outward) is usually initiated directly by you and is designed for quick electronic transfers, often arriving within seconds. Other payment methods may involve scheduled collections, recurring instructions, or longer processing times.

Comparing UK Payment Methods

Before choosing or interpreting a payment on your bank statement, it helps to understand how each UK payment method differs in terms of speed, control, and purpose.

| Payment Type | Typical Speed | Controlled By |

| FPO | Seconds to hours | Account holder |

| Direct Debit | Scheduled collection dates | Company |

| Standing Order | Scheduled by instruction | Account holder |

| BACS | Around 3 working days | Organisation |

| CHAPS | Same working day | Sender |

Looking at these payment methods side by side makes it easier to understand why FPO appears differently from other banking transaction references.

Which Payment Method Is Used for Different Situations?

While payment systems may seem similar at first, each one is designed to support specific types of financial activity and user needs.

- Direct Debit is commonly used for recurring bills such as utilities, subscriptions, and insurance payments.

- Standing Orders work well for fixed regular payments like rent or monthly savings.

- BACS is frequently used for salaries, supplier payments, and bulk transactions.

- CHAPS is normally chosen for urgent or high-value transfers, including property purchases.

- FPO is often preferred for everyday bank transfers because of its speed and flexibility.

“Customers benefit most when they understand which payment system matches their financial purpose rather than focusing only on transfer speed.” — UK Banking Operations Adviser

FPO continues to be widely used because it combines convenience, accessibility, and fast processing, making it one of the most practical payment methods available in UK banking.

Should You Be Concerned If You Do Not Recognise an FPO Transaction?

Most FPO transactions are legitimate, but you should always check any payment you do not recognise. Faster Payments usually move money quickly, so it may become harder to recover funds once the transfer has been completed.

Start by reviewing the payment date, amount, and reference shown on your bank statement. Consider whether it relates to a recent purchase, was authorised by a joint account holder, came from a standing instruction, or appears under a different recipient name than expected.

If you still cannot identify the payment, contact your bank through official channels as soon as possible.

“Customers who report unusual account activity early often have better outcomes because investigations can begin before additional transactions occur.” — Fraud Prevention Specialist

Remaining alert without assuming fraud is usually the most practical approach.

Can an FPO Payment Be Cancelled, Reversed or Traced?

Many people assume bank transfers can be cancelled instantly after sending, but Faster Payments operate differently. Once authorised and processed, reversing the payment may not be automatic.

Banks can sometimes attempt recovery, particularly if an error occurred or fraud is suspected, but success depends on several factors including timing and recipient account status.

If you accidentally transfer funds:

- Contact your bank immediately

- Provide transaction details

- Request payment tracing

- Follow fraud or recovery procedures if applicable

For suspected unauthorised activity, banks may secure your account while investigating.

Although Faster Payments offer speed and convenience, taking time to confirm details before approval remains the safest practice.

How Can You Review and Manage FPO Transactions More Effectively?

Managing FPO on bank statement entries becomes much simpler when you build consistent financial habits and review account activity regularly.

Rather than waiting until the end of the month, checking your statement more frequently helps you recognise transfers, monitor spending patterns, and identify unexpected activity early.

For personal accounts, organising transfers by category can make account tracking easier. For businesses, maintaining clear payment references improves reconciliation and record keeping.

Practical habits that help include:

- Review bank statements weekly rather than monthly

- Check payment references before approving transfers

- Keep digital records of receipts and invoices

- Confirm recipient details before sending money

- Use mobile banking tools to search past transactions

- Match business payments with supplier records

Over time, these practices improve visibility, reduce confusion around FPO transactions, and support better financial management.

Conclusion

Understanding FPO on a bank statement removes uncertainty when reviewing your finances.

In most cases, FPO means Faster Payment Outward, showing that money has been transferred out of your account through the UK Faster Payments system. These payments are widely used for everyday banking activity because they are quick, convenient, and available throughout the week.

Although FPO entries are usually legitimate, unfamiliar transactions should always be checked promptly. Reviewing payment references, confirming recent activity, and contacting your bank where necessary can help protect your account and maintain confidence in your financial records.

Frequently Asked Questions

Does every UK bank use the term FPO on statements?

Not necessarily. Some banks display variations such as Faster Payment, FP Transfer, or Online Transfer, although the meaning is usually similar.

Can an FPO transaction appear as pending before completion?

Yes. Certain payments may remain pending temporarily while security or verification checks are completed.

Are Faster Payments available outside standard banking hours?

Yes. Faster Payments generally operate 24 hours a day, including weekends and bank holidays.

Why does an FPO payment reference sometimes look unfamiliar?

Some businesses appear under legal company names, payment processors, or shortened references rather than customer-facing brand names.

Can joint account holders create FPO transactions?

Yes. Any authorised account holder may initiate Faster Payments depending on account permissions.

Is there a limit on Faster Payment amounts in the UK?

The Faster Payments system supports high transfer values, although individual banks apply their own payment limits.

Can FPO payments be used for business and personal accounts?

Yes. Faster Payments are widely used across both personal and business banking for transfers, supplier payments, and settlements.