What happens when saving money becomes a trigger for increased government scrutiny? Could sharing more personal data with banks become the new normal for millions of UK citizens?

In what is shaping up to be one of the most significant tax enforcement shifts in decades, Rachel Reeves, the UK’s first female Chancellor of the Exchequer, has introduced a far-reaching crackdown aimed at reducing the tax gap and modernising how taxes are collected.

Behind the headlines of economic reform lies a detailed plan to transform the way HM Revenue & Customs (HMRC) interacts with individuals and businesses especially those with savings income.

While the measures are being rolled out quietly, their implications are vast. From requiring savers to submit National Insurance numbers to banks, to automated PAYE deductions for interest earned, Reeves’ tax reforms will impact millions across the UK. Some praise the plan for promoting fairness and efficiency. Others warn of overreach, rising costs, and risks to financial privacy.

This comprehensive breakdown explores the rationale behind the tax crackdown, how the new rules will work, who stands to be affected, and what it all means for the UK’s economic future.

Why Has Rachel Reeves Launched a Tax Crackdown?

The primary driver behind Rachel Reeves’ tax crackdown is the staggering scale of uncollected tax in the UK. HMRC’s own figures estimate that the tax gap stood at £36 billion in 2023.

Reeves, who has positioned herself as a fiscally responsible Chancellor, is seeking to close this gap without raising the main tax rates such as income tax, VAT or national insurance.

The motivation is not only economic but also political. With Labour’s U-turns on public spending creating a projected £50 billion shortfall, there’s mounting pressure on the Treasury to find alternative sources of revenue. Tax enforcement is now being presented as a key component of responsible government.

Reeves’ approach is underpinned by two principles: ensuring that the wealthiest pay their fair share and using modern tools and data to increase compliance.

By investing in HMRC’s enforcement and closing loopholes, the government believes it can raise billions without increasing the tax burden on average earners.

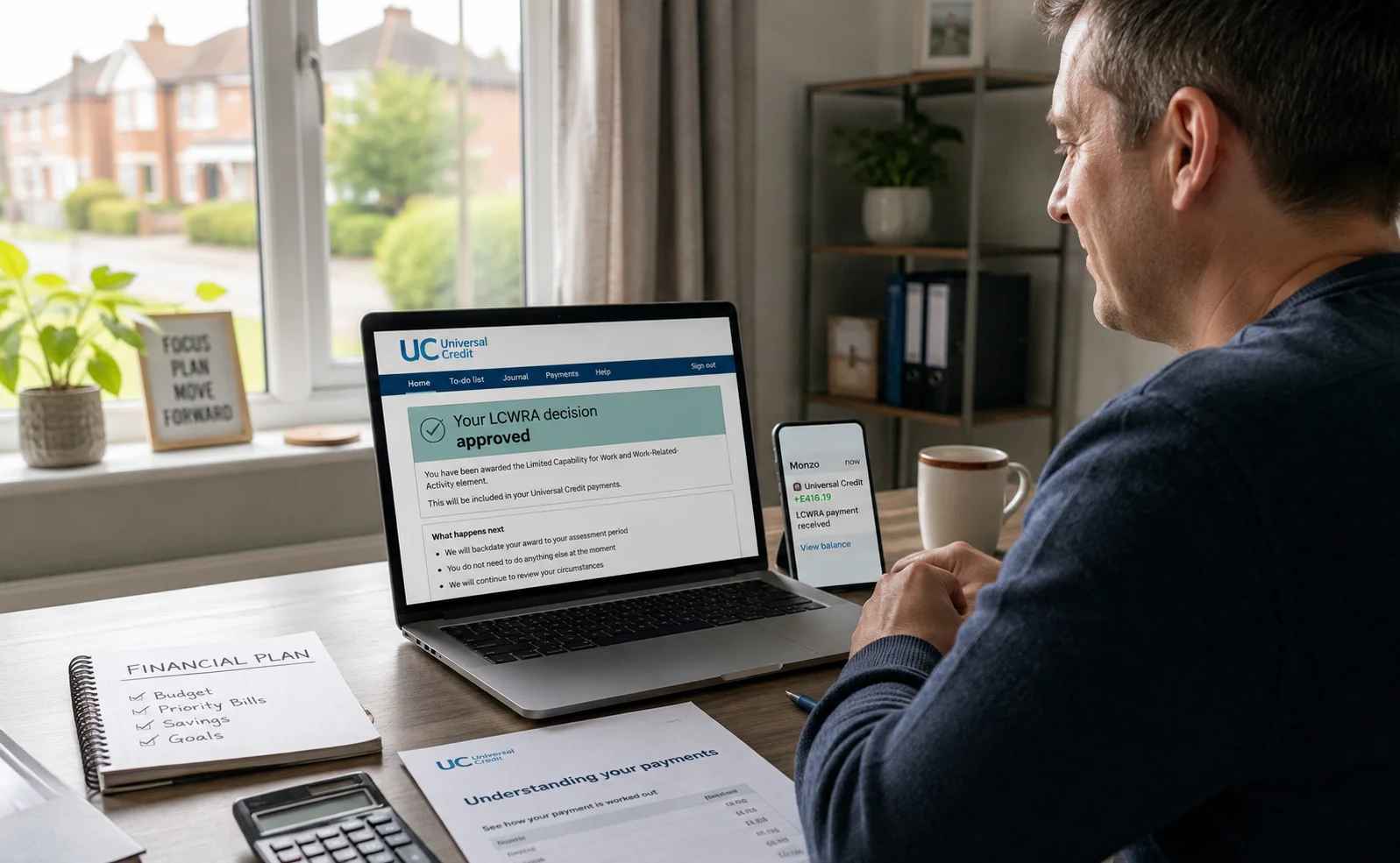

What Are the New HMRC Rules for Savings Accounts?

One of the most notable and controversial changes comes into effect in April 2027. Under these new rules, banks and building societies will be required to collect National Insurance numbers from both new and existing customers with savings accounts.

This change will allow HMRC to link interest income more directly to individual taxpayers, improving accuracy in tax calculations.

The legislation, expected to be introduced in 2026, aims to automatically collect tax on interest earned by adjusting individuals’ PAYE codes, thereby eliminating the need for self-assessment in most cases. For many, tax owed on savings income will be deducted straight from their wages or pension.

Current accounts are not affected by these data-sharing rules for now, but HMRC has not ruled out expanding this requirement in future, raising concerns among privacy advocates.

How Will These Rules Affect UK Savers?

These changes could significantly alter the financial landscape for over 3 million savers. According to HMRC forecasts, 3.35 million savers will earn taxable savings income in the current tax year, with 2.64 million expected to receive a tax bill an increase of 120,000 from the previous year.

At the heart of the issue is the Personal Savings Allowance (PSA). Basic rate taxpayers can earn up to £1,000 in interest tax-free, while higher rate taxpayers are allowed £500. Additional rate taxpayers receive no savings allowance.

Anyone exceeding these thresholds will have their tax calculated and deducted without filing a tax return. While this may seem efficient, it raises questions around transparency and accuracy. Tax experts warn that individuals may not be aware of how much tax they are paying or if it’s correct.

A concern flagged by the Low Income Tax Reform Group and the Association of Taxation Technicians is that savers will be unable to verify HMRC’s figures unless banks are required to share the same data with customers in an understandable format. Without this, errors could go unnoticed for years.

Could the Policy Be Considered an Overreach?

Critics argue that this represents a new level of state intrusion into individual finances. Former Conservative cabinet minister Sir David Davis described the policy as “unsurprising, wrong, and an overreach by HMRC.”

While the government argues that using data from banks will reduce fraud and human error, there is growing discomfort over what some see as the gradual erosion of financial privacy.

The reforms mean that HMRC can assess and deduct tax for years after income was earned up to four years in most cases, six years for careless errors, and up to 20 years if evasion is suspected.

This long window of retrospective enforcement, combined with automated assessments, has raised fears that taxpayers may be penalised without understanding how the figures were calculated, especially in the absence of self-assessment documentation.

What Are the Financial and Administrative Costs of These Changes?

Although the government estimates that the HMRC reforms will cost approximately £35 million to implement, the financial burden on the banking industry is far more substantial.

Industry body UK Finance has warned that the cost to individual banks could reach £10 million each, especially due to the challenges in updating legacy systems and contacting existing account holders.

This is further complicated by low customer engagement. Banks report that as few as 10% of customers respond to letters requesting data, creating logistical hurdles that could delay the reform’s rollout beyond 2027.

There’s also a legal and ethical question about collecting NI numbers from savers under the age of 16, who typically don’t yet have one. Despite this, many children hold savings accounts. The lack of clear guidance on this issue could create confusion for families and financial institutions alike.

How Will Tax Be Collected Under the New System?

Currently, tax on interest income is collected either through self-assessment or, in many cases, not at all due to unreadable or incomplete data shared by banks. HMRC revealed that up to 20% of savings data received is unusable, preventing the automatic collection of tax.

Rachel Reeves’ plan would address this by standardising the reporting process and matching it to individuals via their National Insurance numbers. The system will use real-time data to make PAYE code adjustments, deducting tax directly from monthly pay or pensions.

This streamlined method should reduce the administrative burden for most taxpayers. However, it also means individuals must trust HMRC’s calculations unless they keep detailed personal records of interest earned throughout the year.

Is the UK Following a Global Trend in Tax Enforcement?

The UK is not alone in tightening tax enforcement using technology and third-party data. Other major economies are taking similar steps to close their tax gaps.

| Country | Strategy | Estimated Gains |

| Germany | Enhanced audits and digital reporting | €10 billion annually |

| United States | $80bn IRS investment, AI auditing | $200 billion over 10 years |

| Canada | Cross-border data integration | CAD 3 billion annually |

| United Kingdom | Bank data-matching, PAYE adjustments | £5 billion projected annually |

This international shift reflects a growing consensus: leveraging data and automation is the most effective way to secure public revenue in a globalised, digital economy.

What Can Taxpayers Do to Protect Themselves?

To avoid errors and maintain control over their finances, taxpayers particularly savers should prepare for these changes. Experts recommend keeping a personal record of interest earned across all accounts each year and understanding how savings are taxed according to your income bracket.

Also, it’s important to regularly check communications from HMRC, especially any PAYE code adjustments, and challenge inaccuracies promptly. Although the system will become more automated, the onus is still on the taxpayer to ensure that the data used is correct.

Clearer communication from HMRC and data transparency from banks will be essential to maintaining public trust in the new model.

What Is the Broader Economic Impact of the Crackdown?

If successful, the Rachel Reeves tax crackdown could transform the UK’s revenue system without raising core tax rates. It is forecast to bring in up to £5 billion per year once fully operational, funding critical services such as the NHS, schools, and infrastructure.

It also represents a major step towards modernising the tax system, reducing reliance on self-reporting, and using technology to address long-standing inefficiencies.

By targeting the wealthiest individuals and corporate tax loopholes, the reforms aim to build a fairer system that doesn’t unfairly burden average earners.

However, the real test lies in balancing these ambitions with public perception. Without transparency, fairness, and simplicity, even the most well-intentioned policies risk backlash.

Resource: https://www.telegraph.co.uk/

FAQs

What is the purpose of Rachel Reeves’ tax crackdown?

The crackdown is designed to reduce the UK’s tax gap by improving enforcement, using data from banks, and automating the collection of tax on savings and other income.

Will I need to file a self-assessment for savings income?

Most people won’t. If HMRC has accurate data, tax will be collected automatically through PAYE. However, self-assessment may still apply in complex cases.

How much interest can I earn before paying tax?

Basic rate taxpayers have a £1,000 Personal Savings Allowance. Higher rate taxpayers have £500. Additional rate taxpayers have no allowance and pay tax on all interest earned.

Can HMRC correct my taxes years after the fact?

Yes. HMRC can reassess taxes up to four years later or longer in cases of careless or deliberate behaviour.

Are banks required to give me the same data they send to HMRC?

Currently, no. But tax groups are urging the government to require banks to provide clear, consistent statements to taxpayers.

What happens if I exceed my savings allowance?

Any tax due will be automatically deducted via PAYE if HMRC has sufficient data. You may be notified by letter or see a change in your tax code.

Will children’s savings be affected?

Children under 16 typically do not have National Insurance numbers, which may create administrative issues. The government has yet to clarify how such cases will be handled.

READ NEXT: