March 2, 2026

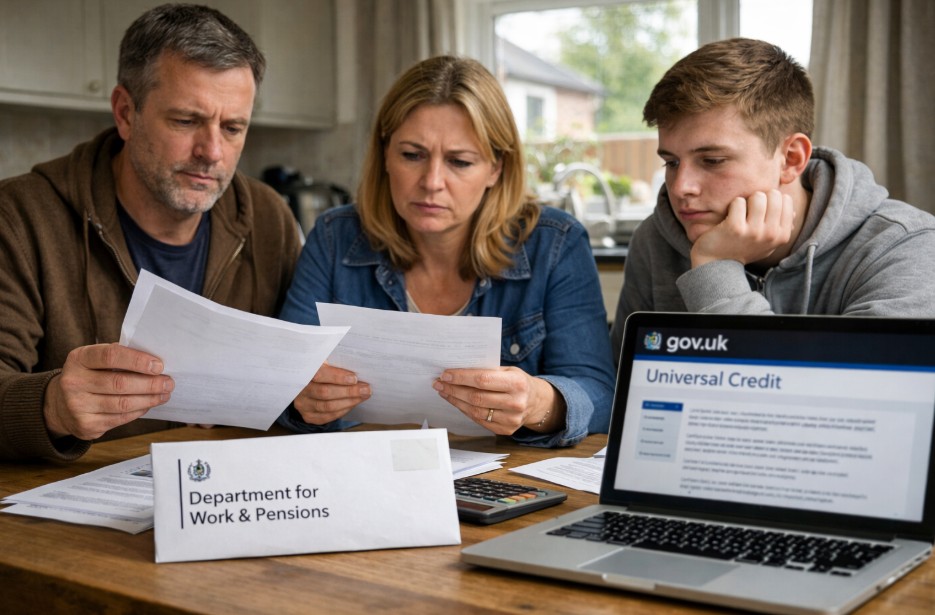

More than 300000 lose DWP benefits after failing to respond to official migration notices as the Government accelerates its Universal...

More than 300000 lose DWP benefits after failing to respond to official migration notices as the Government accelerates its Universal...

Picking HR software shouldn’t feel like playing darts blindfolded. Yet here we are, with HR teams drowning in options, trying...

The narrative surrounding financial technology often centres on disruption, suggesting that traditional banking rails are quickly becoming obsolete. Venture capital...

The HMRC salary sacrifice limit will change from 6 April 2029, introducing a £2,000 annual cap on pension contributions made...

Working from home used to feel like a novelty. Now? It’s the norm for thousands of UK founders building ambitious...

The modern entrepreneurial narrative is dominated by the allure of the “moonshot.” Magazine covers and tech blogs relentlessly celebrate the...

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Curabitur laoreet cursus volutpat. Aliquam sit amet ligula et justo tincidunt laoreet non vitae lorem. Aliquam porttitor tellus enim, eget commodo augue porta ut. Maecenas lobortis ligula vel tellus sagittis ullamcorperv vestibulum pellentesque cursutu.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Curabitur laoreet cursus volutpat. Aliquam sit amet ligula et justo tincidunt laoreet non vitae lorem. Aliquam porttitor tellus enim, eget commodo augue porta ut. Maecenas lobortis ligula vel tellus sagittis ullamcorperv vestibulum pellentesque cursutu.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Curabitur laoreet cursus volutpat. Aliquam sit amet ligula et justo tincidunt laoreet non vitae lorem. Aliquam porttitor tellus enim, eget commodo augue porta ut. Maecenas lobortis ligula vel tellus sagittis ullamcorperv vestibulum pellentesque cursutu.